Beijing’s currency gameplan

Beijing is fortifying an alternative global payment ecosystem

while Washington holds the financial upper hand for now, Beijing is fortifying an alternative global payment ecosystem; it is expected to serve national growth, but not, in the near term, replace the dollar

Hefty tariffs have crippled most PRC–US trade; more blows are likely from Washington in other sectors: PRC experts like Liu Yuanchun 刘元春 and Sun Lipeng 孙立鹏 warn of US restrictions on currency and international payments.

Risk of US sanctions, along with more PRC trade with BRI partners (now over half its total), prompts Beijing and friends to explore other cross-border financial solutions. While still trailing the dollar, euro and pound, the RMB share in global payments reached 3.75 percent in 2024, up 23 percent over 2023. The PRC’s RMB international payment network, CIPS (Cross-Border Interbank Payment System), processed C¥ 175 tn in 2024, up 40 percent over the previous year.

Claiming progress, while warning of heavy lifting ahead, PRC experts urge caution and incrementalism. ‘Doing our own thing well’ is the mantra in this sector, as it is across the board: solutions must remain anchored in PRC needs, not triggered by external (i.e. US) impulses. ‘Exploration’ is again promoted in initiatives to mobilise firms and other market actors. The point is to ‘diversify’ international payments: boosting use of RMB, bilateral local currency settlement, CBDCs (central bank digital currencies), the HKD, etc.

grow, don’t replace

US ‘weaponisation of the dollar’ creates new impetus for global use of the RMB, argues Yu Yongding 余永定 Chinese Academy of Social Sciences. He forecasts that the international currency system may splinter into blocs shaped by quasi-alliances. Global RMB uptake and a trend towards bilateral settlement yield freedom from dollar dominance, concurs Bai Ming 白明 MofCOM Research Institute, offsetting US tariff impact. Given concerns over US debt and SWIFT neutrality, Zhang Ming 张明 Chinese Academy of Social Sciences, suggests offering RMB-denominated safe assets and strengthening CIPS as a reliable alternative payment system.

Recognising RMB ascendence, PRC commentators dismiss hopes of outright replacing the dollar. Still only the world’s second-largest economy, the PRC must act within its means, warns Yu Yongding: the RMB faces a steep climb. It still falls short of the dollar in key areas like global forex reserves and bond pricing, agrees Zhang Ming; the PRC lags in economic, financial, political and military heft. RMB internationalisation should serve national growth, not replace the US dollar. Premature or ill-prepared attempts to do so will, adds Wang Yongli 王永利 China International Futures Co. expose the nation to a host of traps and risks.

experiment and diversify

Prudence aside, reducing dollar reliance remains a long-term interest. Pundits and policy texts converge on stepping up policy pilots and diversifying approaches.

Cases in point run to central bank currency swaps. The PBoC has signed over 40 such pacts with global partners (amounting to some C¥ 4.31 tn), foundational to using local currencies and the yuan in trade and investment. Major yuan-denominated commodity deals in energy and minerals are deemed promising for settlement and pricing.

Despite domestic market constraints, such moves are underway in LNG. A buyer, the PRC remains limited by seller currency preferences, laments Liu Yun 刘云 Kunlun Policy Research Institute. RMB payments, he suggests, should be required or at least encouraged, for goods in which the PRC holds sway: shipbuilding, critical minerals, batteries... With ever tougher controls on some of these exports, this is not beyond reach.

More precise moves would entail an extensive overhaul of PRC economic and financial norms. ‘Doing our own thing well’ is yet again at a premium. This presumes a more resilient and market-oriented economy, featuring stable growth, tech and trade. These are key to promoting the global uptake of RMB, argues Li Daokui 李稻葵 Tsinghua University School of Economics and Management. Such stability in growth, tech and trade entails a more open and mature financial market, adds Zhang Ming. Recent policy moves display this view

a PBoC action plan pledging efficiency in cross-border financing

a Central Committee and State Council Opinion calling for greater financial opening in FTZs

expanding futures products, easing external dealings

Financial trade volume, a key index of RMB acceptability, currently lags behind RMB payments and settlements, notes Wang Yongli. To reverse this, the capital market needs to be multi-tiered, enabling overseas RMB holders to invest in wider categories of products, argues Liu Ying 刘英 Renmin University Chongyang Institute for Financial Studies.

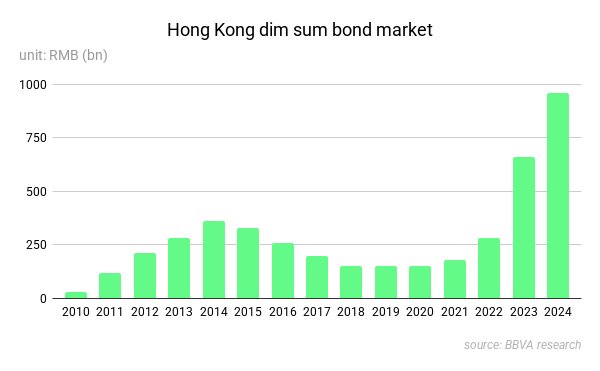

Make better use of Hong Kong, urges veteran economist, Huang Qifan 黄奇帆 China Institute for Innovation and Development Strategy, linking the PRC to world markets. Taking the cue, reports BBVA, the largest offshore RMB centre saw RMB bond and loan volumes lift in 2024 over 2023. Given the notable appointment of a high-level PRC finance official (Qi Bin 祁斌 a former China Investment Co. deputy general manager) to Beijing’s Hong Kong representative office in late 2024, moves are on the cards for it to serve national financial priorities.

Responding to claims that exchange rate and capital controls are the root of slow global uptake of RMB, Yu Yongding insists that the PRC can internationalise the yuan under existing conditions, albeit as a long-term national goal.

Echoing this, Peng Wensheng 彭文生 China International Capital Co., suggests that with greater global financial regulation reminiscent of the Bretton Woods era, capital controls may hinder RMB globalisation less.

With the world weary of financialisation, this globalisation drive should prioritise ‘real’ economies and trade. Against rising headwinds, the PRC should liberalise the capital account prudently, warns Zhang Ming.

leverage trade and investment

Free trade provides ground for local currency settlements, argues Chi Fulin 迟福林 China Institute for Reform and Development, urging broader trade liberalisation in BRICS. Raise the RMB settlement ratio first with BRI and ASEAN partners, suggests Huang Qifan, as trade ties deepen. To boost global yuan uptake, Beijing may come to rely less on export-driven growth. Yuan outflows would be triggered by stepping up imports and consumption, argues Zhang Yansheng 张燕生 Academy of Macroeconomic Research. With pressure to reduce trade imbalance and respond to US tariff hikes, more moves to open PRC markets may be on the horizon.

Growing PRC overseas investment amid tariff headwinds holds potential for further uptake of RMB. This would bolster firms’ financial security, reducing forex risks, argues Wang Zhiyi 王志毅 Cross-Border Financial Research Institute. Over 70 percent of surveyed overseas PRC firms now settle some cross-border trade using RMB, following a joint Renmin University and Bank of Communications report, with most arguing for more policy support. Taking the hint, a recent PBoC action plan backed RMB settlement for PRC state-owned and private firms venturing abroad.

Given that some Global South states remain underdeveloped, lacking the purchasing power to absorb PRC products and capacities, Beijing should drive their growth with financial support, suggests Zhai Dongsheng 翟东升 Renmin University of School of Global and Area Studies. The RMB will be increasingly used in BRI projects, forecasts Zhang Jianping 张建平 MofCOM Research Institute.

payment goes digital

CIPS remains reliant on global banks to conduct transactions, exposing the PRC and CIPS users to US sanctions risks, argues Chen Xin 陈欣 Shanghai Jiaotong University School of Finance. A decentralised CBDC like the digital yuan he adds, cuts out the intermediary, allowing for peer-to-peer transfers using blockchain. Combining the digital yuan with CIPS could happen in future.

The mutli-CBDC ‘mBridge’ is a joint pilot of the Hong Kong, Mainland China, Thailand and the UAE central banks. In a 2022 six-week pilot, it settled HK$171 million in 160 transactions, cutting cross-border transfers from days to seconds. It entered the Minimum Viable Product stage in mid-2024.

mBridge upholds central bank sovereignty, as it manages the cross-border exchange/transfer of participating local currencies only. This can then work with a decentralised system empowering members to manage their respective blockchain nodes, claims Zhou Xiaochuan 周小川 PBoC former governor. Its goal is to meet the growing demand of cross-border payment channels for ‘quasi-strong currencies’ like RMB, HKD, AED and THB, adds Zhou, noting that this goal is not in conflict with the USD per se.

Building ‘new tech’-based cross-border financial infrastructure is a Third Plenum priority, explains Mu Changchun 穆长春 PBoC Digital Currency Research Institute: mBridge needs improvement. Admitting political, economic and technical challenges remain, Wen Jing 文晶 Tsinghua University Centre for International Strategy and Security argues mBridge lays the groundwork for a similar local currency payment system for BRICS states. More discussion of local currencies is expected at the next BRICS summit (July 2025).

friction ahead

Beijing’s drive for tech self-reliance and trade diversification was catalysed by US trade and high-end materials sanctions in 2018. Rather than stalling progress, they sharpened Beijing’s resolve. Now, as the US signals broader tariffs, economic decoupling and curbs on PRC currency and financial flows, Beijing strives to develop a robust payments network with partners—further diminishing its ties to the US. Trump 2.0 has squeezed relations with the PRC to crisis point: the more it squeezes, the slipperier its grip, and the harder it needs to squeeze. Against these unilateral and chaotic tactics, Beijing appeals as more reliable and inclusive—preaching ‘genuine multilateralism’, hinting at minilateral alternatives.

currency wonks

Zhang Ming 张明 Chinese Academy of Social Sciences Institute of Finance deputy director

Currencies wield more clout via pricing than settlement, insists Zhang: the yuan should hence be focused on the former, above all in industry and supply chains. Beijing should, he suggests, bolster RMB cross-border financial infrastructure: overseas presence of commercial, RMB agent and cross-border clearing banks; domestic FTZs should pioneer RMB internationalisation experimentation.

Global finance economist Zhang specialises in capital flows and RMB internationalisation. A veteran of asset management and investment research, he is a deputy director and research fellow at the Institute of Finance, Chinese Academy of Social Sciences.

Zhou Xiaochuan 周小川 former PBoC governor

Deeper ties between Asian economies stimulate demand for cross-border payment channels, argues Zhou. Due to liquidity shortages, misaligned central bank policies and monetary independence concerns, ‘strong’ currencies like the USD are in decline. Pan-Asia cross-border payment protocols like mBridge prosper as a result. Choice between currencies boils down to efficiency, cost, security and user preferences. For Zhou, dollar dominance as the top reserve and trade currency is ultimately decided in Washington.

Mastermind behind internationalising Chinese finance, including the RMB, Zhou is also its human face. A protégé of veteran reformer Wu Jinglian 吴敬琏, Zhou pursues a long-term, global vision. His widely read essay, penned after the global financial crisis, argues for an end to dollar-dominance and the establishment of a global reserve currency. Domestically, Zhou has championed financial liberalisation, allowing capital account opening, meeting international prudential standards, marketising interest rates and moving away from policy-driven lending and soft budget constraints. In the lead-up to SDR inclusion, other authorities viewed his advocacy of faster capital account opening sceptically. Agreed on the goal, they diverge on the timetable and sequencing. Look to his speeches at key political junctures, particularly the upcoming NPC in March 2016, for the following major reforms to the financial system.

Wang Yongli 王永利 China International Futures Co. general manager

Local currency settlement in principle curbs exchange rate risks and payment settlement costs, notes Wang. Yet this may entail increasing those of one’s partners. He adds that inequality between the two may result in the party with more power and influence standing to benefit.

Veteran banker Wang spent 25 years at Bank of China, rising to a vice chief executive before stepping down in 2014. Joining Shenzhen private pharma giant Neptunus Group as chief economist in early 2019, he is now general manager at China International Futures Co., the PRC’s largest and oldest futures brokerage firm.

| A guest post by

|