Beijing is talking about the real economy again

Beijing has swung its economic message back to the real economy. Through 2024 and 2025 the mood ran the other way. In late 2024, Zhou Hanmin 周汉民, a CPPCC standing committee member, argued that the virtual economy held ‘infinite potential’, with the metaverse and tokenised assets as its next frontier. The mood grew more exuberant through 2025: a second-year equity rally, an AI build-out, and a rush to turn data and real-world assets into claims that investors would finance.

Qiushi, the Party’s flagship theoretical journal, gave much of its 16 May 2026 issue to the real economy. It carried three pieces: a compilation of Xi Jinping’s remarks on the real economy, 2016–25; an article by Li Lecheng 李乐成 MIIT (Ministry of Industry and Information Technology) on securing the real economy on a manufacturing base; and a notably self-critical piece by Mo Wangui 莫万贵 PBoC (People’s Bank of China) financial research institute on the gaps in financial service to industry.

As the global AI surge raises the stakes, the three pieces amount to a renewed attempt to sort the forms of growth that count as productive from those that risk drawing capital, talent and policy attention away from the industrial base. Beijing’s posture is best read as conditional support: the virtual economy is to be harnessed rather than rejected, with finance, data and digital activity kept tied to productive allocation.

2006–25 manufacturing share of PRC GDP

never quite settled

The line between real and virtual is older than it looks. The virtual economy, in the economic sense, refers to Marx’s idea of ‘fictitious capital’ in ‘Das Kapital’: claims on future income that circulate through markets without directly producing goods. The term means something narrower than the online activity it now suggests. The concept was brought into PRC policy rhetoric by Cheng Siwei 成思危, former NPC Standing Committee vice chair in the late 1990s after the Asian Financial Crisis; in current usage, it points to finance, real estate and speculative or capitalisation-driven activity.

The framing was contested at the top from the start. In 2002, later central-bank governor Yi Gang 易纲 (2018–23) co-authored an essay titled plainly ‘Finance is not virtual economy’, and Zhou Xiaochuan 周小川 PBoC governor (2002–18) acknowledged at the 2021 Lujiazui Forum that the debate had never been formally resolved. Beijing acted on it regardless: the 2017 National Financial Work Conference made finance serving production a rule, the 2023 Central Financial Work Conference codified it among the ‘eight upholds’ of finance with Chinese characteristics, and the 15th 5-year plan recommendations placed strengthening the real-economy foundation first among 12 strategic tasks.

The May 2026 compilation is the latest reinforcement, republishing Xi’s 2024 warning that finance ‘enamoured of self-circulation and self-expansion’ becomes water without a source, with crisis to follow.

western lessons, PRC constraints

The cautionary reference is the West. Taking lessons from the Asian and Global Financial Crises, PRC policy thinkers have long read western deindustrialisation and financialisation as a warning: once manufacturing is offshored and finance detaches from production, economies can gain asset wealth and high-end services while losing industrial depth, mid-income employment and resilience.

Quan Heng 权衡 Shanghai Academy of Social Sciences Party secretary has put it bluntly, arguing that Shanghai cannot build its ‘five centres’ (the city’s plan to become an international hub for economy, finance, trade, shipping and technology innovation) by shifting wholly into services, and must hold a share of high-end manufacturing rather than follow New York or London. Writing in the same vein, Li Lecheng quantified the concern: the PRC’s manufacturing share traces an inverted U, peaking at some 32 percent of GDP in 2006 and settling at 24.7 percent in 2025, which he frames as stabilising within a reasonable range. The aim is to keep manufacturing in range while raising its quality, with services, finance and digital activity treated as inputs into upgrading rather than substituting it. The wider question, on Quan’s account, is one of allocation rather than sector: with the room to add capital and labour largely exhausted, growth must turn on total factor productivity and how well resources are used, and the danger is misallocation, not finance as such.

where the boundary falls

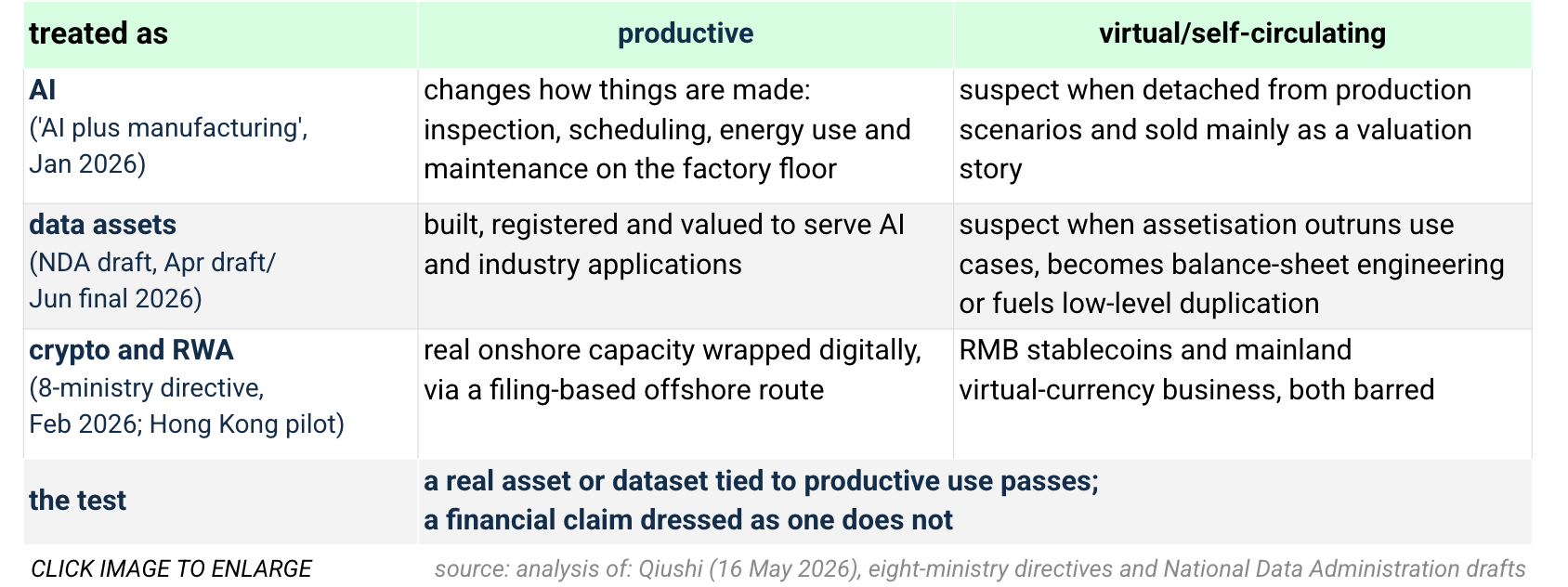

The distinction carries directly into policy. Equating the digital economy with the virtual economy is a misconception, warns Mei Hong 梅宏 CAS academician and China Computer Federation president: software, telecoms and electronics manufacturing belong to the real economy, and industrial digitalisation does too when it serves production. This logic underpins the ‘AI plus manufacturing’ program issued by eight ministries in January 2026, which sets targets for 2027 in industrial agents, 100 high-quality industrial datasets, and 500 application scenarios. The official framing treats AI as productive when it changes production functions, solving problems in inspection, scheduling, energy efficiency and maintenance, rather than when it generates valuations.

Data assetisation is the harder new boundary. Beijing wants data to be a factor of production, which requires registration, valuation and tradable rights, each of which also makes data more financial. The National Data Administration’s April 2026 consultation draft on industry datasets encourages exploring data pledging, equity contribution, securitisation, trusts and insurance, with 2026 designated a year of ‘data value release’.

Crypto sits on the same line. The eight-ministry directive on virtual-currency risks issued in February 2026 maintains the mainland ban on virtual-currency business and bars RMB stablecoins, but for the first time defines real-world-asset tokenisation and opens a filing-based offshore route, but only where the token is backed by real onshore productive capacity. Hong Kong is the testing ground, though two licences granted from 36 applicants in April point to a narrow gate.

The test running through all three is consistent: a real asset wrapped digitally counts as productive, while a financial claim dressed as one does not.

the sorting test: what Beijing counts as productive

capital with a destination

The same logic governs finance, which is to be directed rather than shrunk. Two impulses run in parallel: pushing capital toward favoured uses, and stopping it from circulating on itself.

On the first, the organising idea since 2024 has been ‘patient capital’: a September 2024 guiding opinion and January 2025 implementation plan on long-term funds entering the market; an April 2025 rise in the insurance equity-allocation ceiling from 30 to 35 percent; longer, three-to-five-year evaluation cycles for state insurers and an April 2026 fund-manager appraisal rule binding pay to long-run results; and government guidance funds with a C¥12.84 tn (~US$1.76 tn) target by end-2024.

Lending under the ‘five articles’ (technology, green, inclusive, pension, digital finance) reached C¥108.8 tn (~US$15.5 tn) by end-2025; direct financing is pushed through the STAR Market, ChiNext and the Beijing exchange. As Wu Qing 吴清 CSRC chair put it at the 2025 Lujiazui Forum, the PRC capital markets remain short of long-term, risk-tolerant capital, and the institutional task is to foster it.

The second impulse is the more revealing. Beijing treats ‘capital idling’, money looping inside the financial system through arbitrage rather than reaching firms, as the operational twin of ‘turning from real to virtual’. The central bank has moved repeatedly against it. In April 2024 a PBoC-led panel of banks scrapped ‘manual interest top-ups’, a back-door sweetener on large corporate deposits that had money sitting in banks for yield rather than reaching firms. It went on to curb structured deposits and interbank arbitrage and to tighten interbank-deposit discipline, draining some C¥4.3 tn (~US$590bn) from large banks’ interbank books between December 2024 and January 2025. Behind these moves is a deeper target. PBoC governor Pan Gongsheng 潘功胜 has criticised the ‘scale obsession’ that drives banks to expand through irrational competition and blunt how rate cuts pass through to lending.

margin leverage tops its 2015 bubble-era peak

Note: margin financing crossed its 2015 bubble-era peak in September 2025, a sign of the ‘money chasing money’ in equities that Beijing wants to rein in.

the limits of the line

The debate is not settled in practice, and Beijing says so itself. In the same May Qiushi issue, Mo Wangui concedes that capital crowds into late-stage projects and inflates valuations while early-stage firms go short, that banking ‘involution’ is eroding interest margins, and that long money stays long without being long-invested.

The line between productive allocation and self-circulation is easier to assert than to enforce. The harder question is not whether Beijing can push capital toward the real economy. That machinery now exists. It is whether the real economy can absorb and use what is pushed toward it fast enough to vindicate the doctrine.

real and virtual, in person

")

Li Lecheng 李乐成 | Party Secretary and Minister of the Ministry of Industry and Information Technology (MIIT)

For Li, the test of the artificial-intelligence wave is whether it changes how things are made rather than how they are valued. He casts AI as a ‘key variable’ becoming a ‘strong increment’ for the real economy only insofar as it is put to work on the factory floor, in design, scheduling and quality inspection, and frames the task as a ‘two-way rush’ in which manufacturing supplies the datasets and application scenarios that anchor models to production. By end-2025, he notes, AI had reached over 30 percent of large industrial firms, and the PRC was producing over 300 humanoid-robot models. His insistence that AI remain ‘used by people, serving people and controlled by people’, and that technological innovation fuse with industrial innovation, marks the same line the doctrine draws elsewhere: digital capability counts as productive when it lifts output, and becomes suspect when it floats free as an asset story of its own.

Known as a champion of ‘new-type industrialisation’ and the drive to keep manufacturing as the bedrock of the real economy, Li argues China’s manufacturing is ‘large but not strong’ and must deepen the fusion of technological and industrial innovation. He is Party Secretary and Minister of Industry and Information Technology and a member of the 20th Central Committee, becoming MIIT Party secretary in February 2025 and minister in April 2025. An engineer who rose from factory technician to plant director in Hubei, he later served as governor of Liaoning, executive vice governor of Hubei, party secretary of Xiangyang, director of Hubei’s DRC and mayor of Yichang.

Zhou Hanmin 周汉民 | Standing Committee Member of the National Committee of the CPPCC

Zhou casts the virtual economy as a frontier of historically unprecedented scale: by 2000, he notes, it already stood at five times world GDP, and in the digital era that trajectory accelerates, with the metaverse, tokenised assets and blockchain-enabled finance opening wholly new spaces for economic activity. Artificial intelligence and virtual reality are, on his account, the infrastructure that gives the virtual economy productive legitimacy rather than speculative overlay. He acknowledges the risks: greater market volatility, data-security exposure and the difficulty of regulating activity that crosses borders as readily as it crosses asset classes. Yet his prescriptions converge quietly with the doctrine he seems to challenge: he calls for financial innovation to be matched to the real economy’s needs and for capital to be redirected toward technology, advanced manufacturing, green development and small firms. The frontier he champions must, on his own account, stay anchored in productive purpose.

A longstanding advocate of opening and of the virtual and digital economy’s potential, Zhou is known for his early scholarship on the WTO and GATT, on which he co-authored books in the 1990s. He is a standing committee member of the CPPCC, president of the Shanghai Public Diplomacy Association and a vice chair of the China National Democratic Construction Association’s Central Committee. His career has centred on Shanghai’s external economic engagement and trade diplomacy.

context

24 May 2026: Yi Gang 易纲 restates that the real economy is finance’s foundation and finance a ‘producer service‘

16 May 2026: Qiushi 2026/10 runs Xi Jinping’s ‘On strengthening the real economy’, with Li Lecheng 李乐成 and Mo Wangui 莫万贵

17 Apr 2026: AMAC finalises a fund-manager appraisal rule tying pay to long-run results

15 Apr 2026: the National Data Administration issues a consultation draft on industry datasets and names 2026 a year of ‘data value release’

6 Feb 2026: eight ministries ban RMB stablecoins and first define RWA tokenisation (PBoC doc 42/2026)

Jan 2026: eight ministries issue the ‘AI+ manufacturing’ special action plan with 2027 targets

Jun 2025: at the Lujiazui Forum, CSRC chair Wu Qing 吴清 calls capital markets short of ‘patient capital’

Apr 2025: the NAFR raises the insurance equity-allocation ceiling from 30 to 35 percent

Mar 2025: NDRC chair Zheng Shanjie announces a National Venture Capital Guidance Fund

Jan 2025: six ministries issue the implementation plan on long-term funds entering the market

Nov 2024: Zhou Hanmin 周汉民 tells a forum the virtual economy holds ‘infinite potential’

Sep 2024: the Central Financial Office and CSRC issued a guiding opinion on long-term funds entering the market

Apr 2024: PBoC-led panel of banks scrapped ‘manual interest top-ups’ to curb capital idling

Oct 2023: the Central Financial Work Conference sets the ‘eight upholds’ and the ‘five articles’

Jun 2021: at the Lujiazui Forum, Zhou Xiaochuan 周小川 says the real/virtual debate was never resolved

Jul 2017: the fifth National Financial Work Conference makes finance serving the real economy a rule

2002: Yi Gang 易纲 co-authors ‘Finance is not virtual economy’, disputing the real/virtual split